Can a Company Change Its Inventory Method Each Accounting Period

Beginning inventory Purchases - Ending inventory Cost of goods sold. A company should not change the inventory costing method each period in order to maximize net income.

What Are The Different Inventory Valuation Methods For Small Businesses Hourly Inc

To adjust the Inventory account balance from a debit balance of 35000 to a debit balance of 40000 the following adjusting entry will be needed.

. Inventory change is part of the formula used to calculate the cost of goods sold for a reporting period. The nature of change in accounting policy it will show what has been changing. 47 121 50 2 Chat.

Solutions for Chapter 5 Problem 6DQ. This is an example of the disclosure principle. You can use a different accounting method for each business.

Lets also assume that the Purchases account showed a debit balance of 200000 for the year. 1446-1 e 3 i requires that in order to obtain the Commissioners consent to make a method change a taxpayer must file a Form 3115 Application for Change in Accounting Method during the taxable year in which the taxpayer desires to make the proposed change. However this freedom of choice does not include changing inventory methods every year or so especially if the goal is to report higher income.

A change in accounting principles is a change in a method used such as using a different depreciation method or switching between LIFO to FIFO inventory valuation methods. The consistency principle states that a business should use the same accounting methods from period to period. Suppose you are analyzing a companys net income over a two-year period in which there was an increase in net.

The inventory change figure can be substituted into this formula so that the replacement formula is. Under WAC a company can manipulate its income near the years end by how much inventory it buys. Step 1 of 4.

Company can have a net loss if its expenses absent cost of goods sold are greater than its gross profit from sales of merchandise. The reason for a new policy which can provide more reliable and relevant financial information if the change is voluntarily made. Heres a couple of reasonsexamples why profit is subjective1 Inventory valuation methods LIFOFIFO average cost etcChange the inventory valuation method and.

According to the consistency accounting principle a company should follow same accounting method every year so that its financial statements can be compared. It allows to make change in the accounting method only if the changed accounting method shall improve its financial reporting. 300-400 words no format but work must be citied.

Explain300-400 words no format but work must be citied. Financial Accounting Fundamentals 5th Edition Edit edition This problem has been solved. Continuous switching of methods violates the accounting principle of consistency which requires using the same accounting methods from period to period in preparing financial statements.

If company changes its inventory valuation method from FIFO to weighted average method then it is basically changing the principle of valuation as FIFO follows a particular cost flow assumption whereas weighted average method uses weighted average of the cost at which inventory was held at the beginning of the period and cost of the goods. Answer 1 of 5. Can a company change its inventory method each accounting period.

It means a lot of work for their staff in revaluing and checking the transactions and creates a valuation mess in their financials. Thus the cost of goods sold is largely based on the cost assigned to ending inventory which brings us back to the accounting method used to do so. Can a company change its inventory method each accounting period.

The consistency principle states that businesses should use the same accounting methods and procedures from period to period. The amount adjustment in the current and prior periods. Beginning inventory Purchases - Ending inventory Cost of goods sold.

An alternative to the FIFO method is the last-in first-out cost of inventory. The account Inventory Change is an. A change in accounting principles refers to a business switching its method of compiling and reporting its financials.

Accounting principles for inventory valuations. With LIFO the most recent merchandise is sold before the products previously sitting on the shelves. Consistency helps investors and creditors compare a companys financial statements from one period to the next.

Each method will also change slightly based on whether the company uses a periodic or perpetual inventory system. Exhibits 4 and 5 illustrate how the company would adjust its retained earnings to reflect a change in inventory methods. Credit Inventory Change for 5000.

It can use the method of accounting used in its. Inventory Change in Accounting. Changing the inventory method each period would violate the accounting concept of.

Changing the inventory method each period would violate the accounting concept of consistency. There are several possible inventory. Justification for the change and the effect of the change on net income be disclosed in the notes or in the body of a companys financial statements.

The full formula is. But the most important fact is that inventory method. Under the periodic inventory system there may also be an income statement account with the title Inventory Change or with the title Increase Decrease in Inventory.

Exhibit 4 shows the 20X6 adjustment while exhibit 5 reflects adjustments in comparative statements for. Can a company change its inventory method each accounting period. The basic formula for determining the cost of goods sold in an accounting period is.

No business is separate and distinct unless a complete and separate set of books and records is maintained for each business. Question is why would the company want to change the valuation method every accounting period. Can a company change its inventory method each accounting period.

Overall though the averaging process in WAC diminishes the timing effects associated with the purchase of inventory. Quantify the amount impact by the change in each financial line items. Can a company change its inventory method each accounting period.

A company changes its inventory costing method each period in. This account is presented as an. Inventory change is the difference between the amount of last periods ending inventory and the amount of the current periods ending inventory.

Specifically the company will either choose between a variety of generally. When a partnership changes its tax year a short period return must be filed. 2015-13 603.

Debit Inventory for 5000 and. Discuss 3 Inventory valuation methods that can be applied in terms of the International Financing Reporting Standards In your discussion examine when it is appropriate to use each of the methods Include an example to illustrate how different.

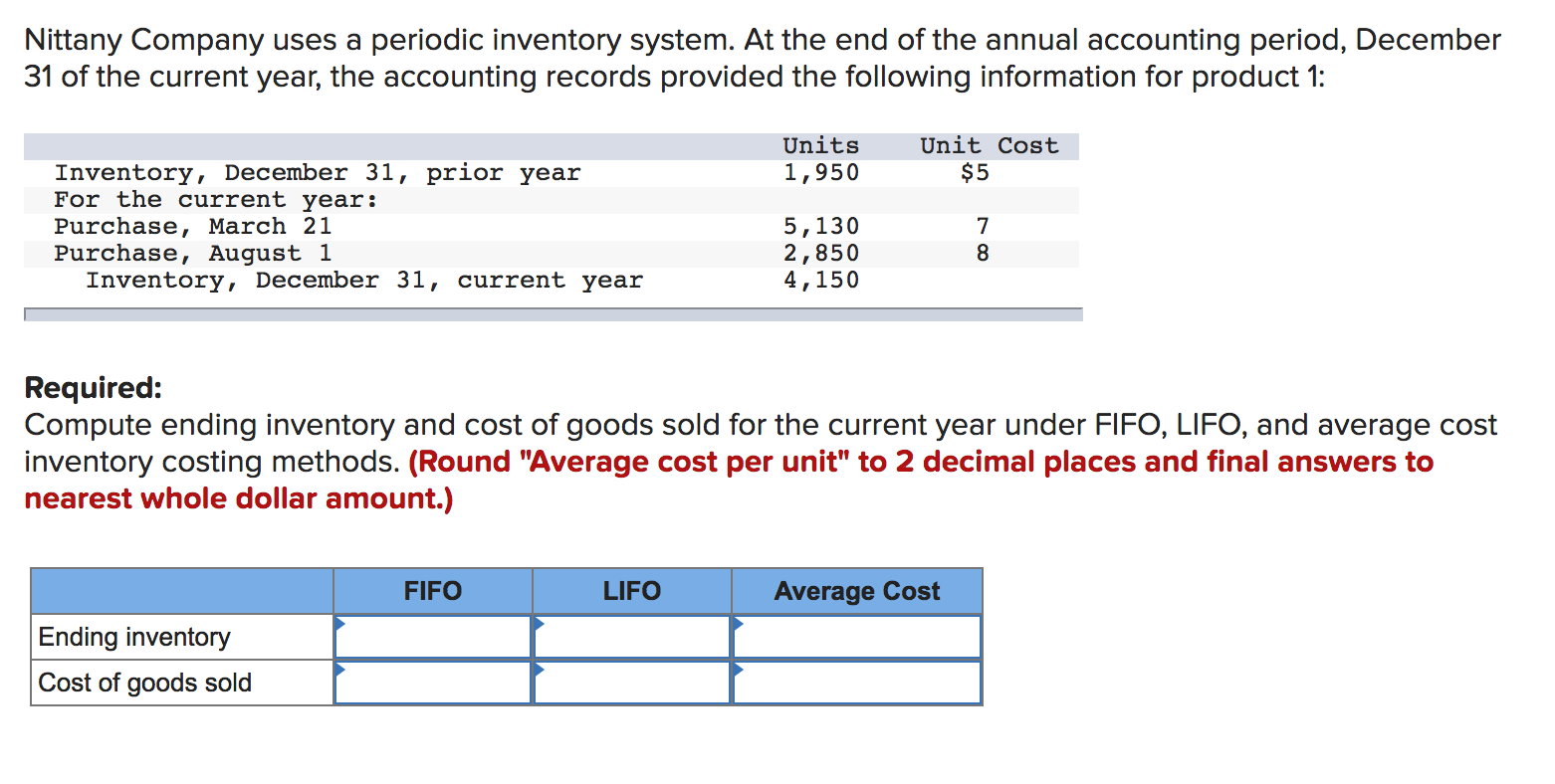

Solved Nittany Company Uses A Periodic Inventory System At Chegg Com

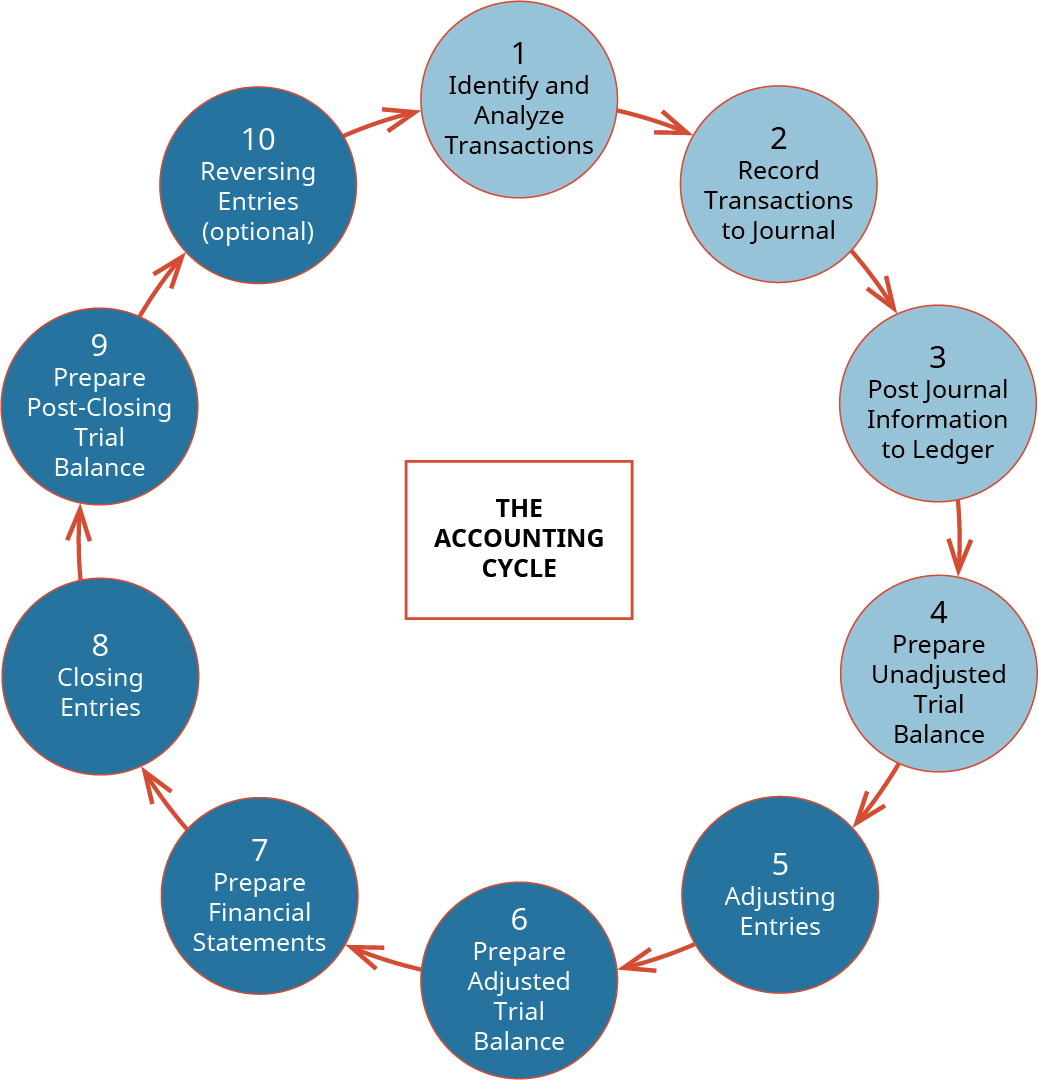

Define And Describe The Initial Steps In The Accounting Cycle Principles Of Accounting Volume 1 Financial Accounting

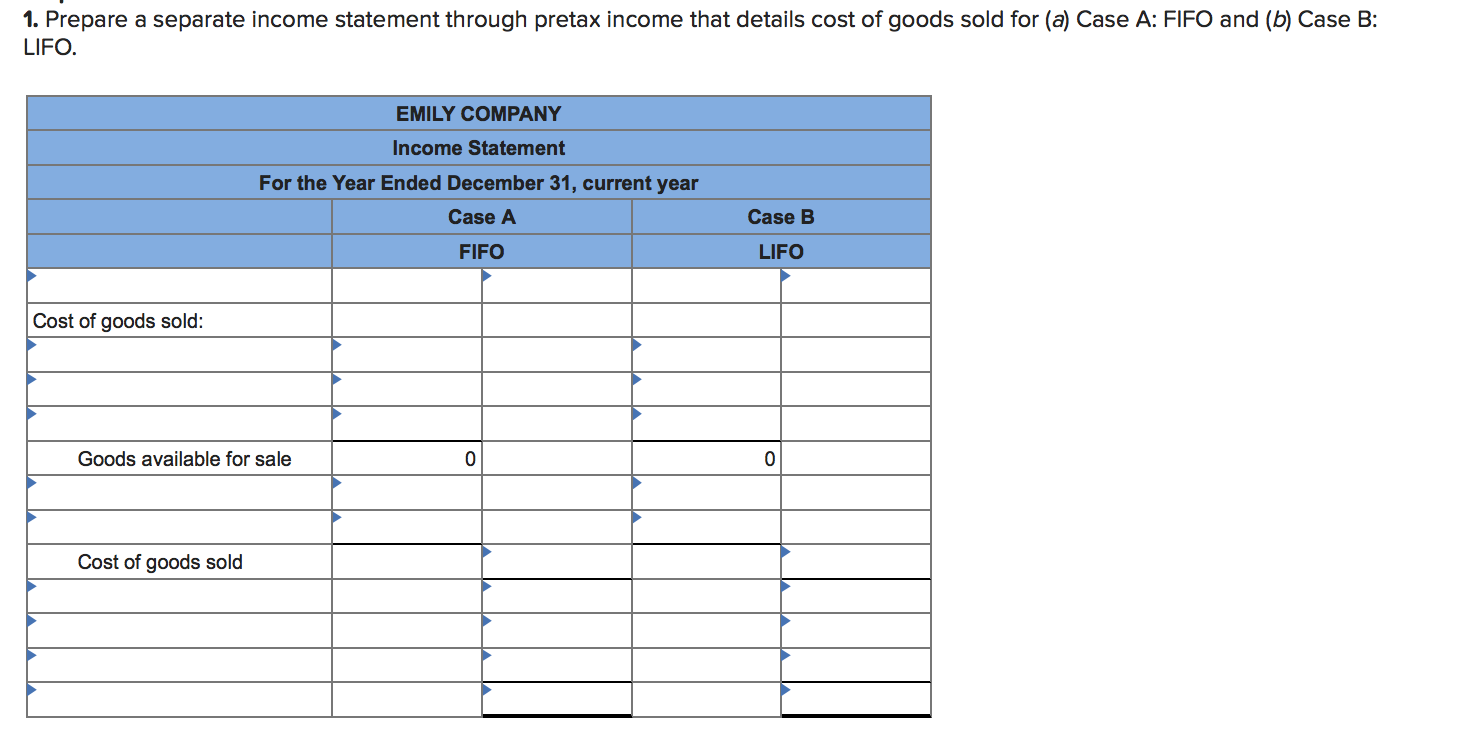

Solved Emily Company Uses A Periodic Inventory System At Chegg Com

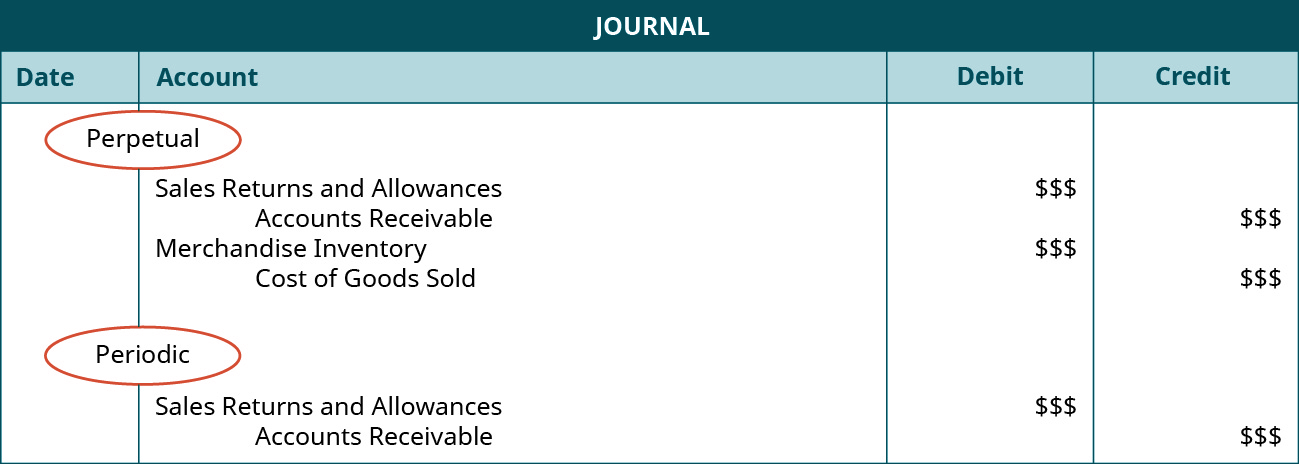

Compare And Contrast Perpetual Versus Periodic Inventory Systems Principles Of Accounting Volume 1 Financial Accounting

Comments

Post a Comment